I’ve been building FinTech products for the better part of 10 years and this is at the heart of every bank conversation I’ve ever had. The discussion always goes in different directions.

I asked this question on Twitter and at the time the question was somewhat rhetorical. I thought the answers would be more consistent depending on the use case/partnership. The answers surprised me and went much higher level than I was anticipating.

In less than 24 hours I received a masterclass on the subject from some friends, an auditor, a former bank regulator, and an investment banker. My somewhat rhetorical question alluded to my own flaw in the approach of defining value. I’ve been going too low level!

One thing was consistent in the answers and in the ongoing communication via DM and e-mail: net interest margin. Even if we agreed that it wasn’t particularly useful in one analysis, there was always agreement that it was useful when considering how a bank might prioritize a potential partnership.

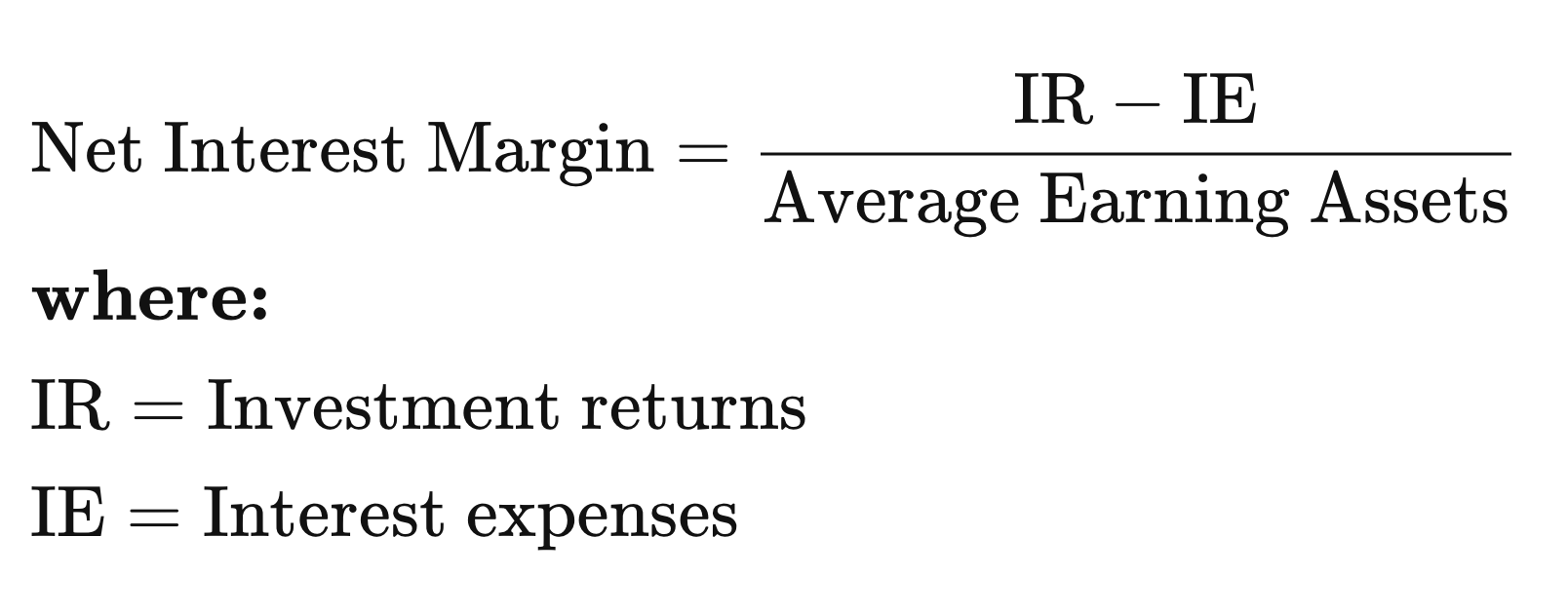

Net Interest Margin

Simply put. A bank pays its client for deposits and this is a cost center for the bank. It then turns those deposits into assets that it makes money on them. Bonds, loans, etc etc.

Here is the Investopedia definition:

Net interest margin (NIM) is a measurement comparing the net interest income a financial firm generates from credit products like loans and mortgages, with the outgoing interest it pays holders of savings accounts and certificates of deposit (CDs)

In a nutshell, income after expenses.

Understanding NIM value to a FI

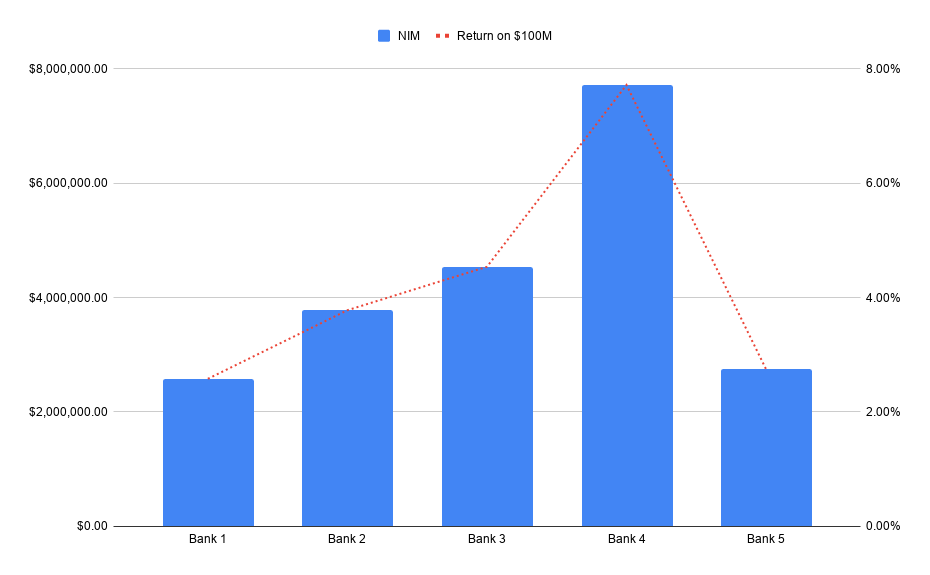

You can do it however you want really but here’s how I think about it after the past few days. I’ve decided to look at the last 5 years and apply the appropriate trend line going forward.

So let’s assume that the target partnership produces $100M in new deposits for a bank. The NIM can help us see what those are hypothetically worth.

Generating millions of dollars in revenue from non-interest generating services like transactional services is pretty common. Throw in interest generating income and it’s clear why the convergence between FinTechs and banks is now normal.

Banks don’t have to own the entire technology stack and FinTechs don’t need to own the entire regulated infrastructure stack for everyone to do well.

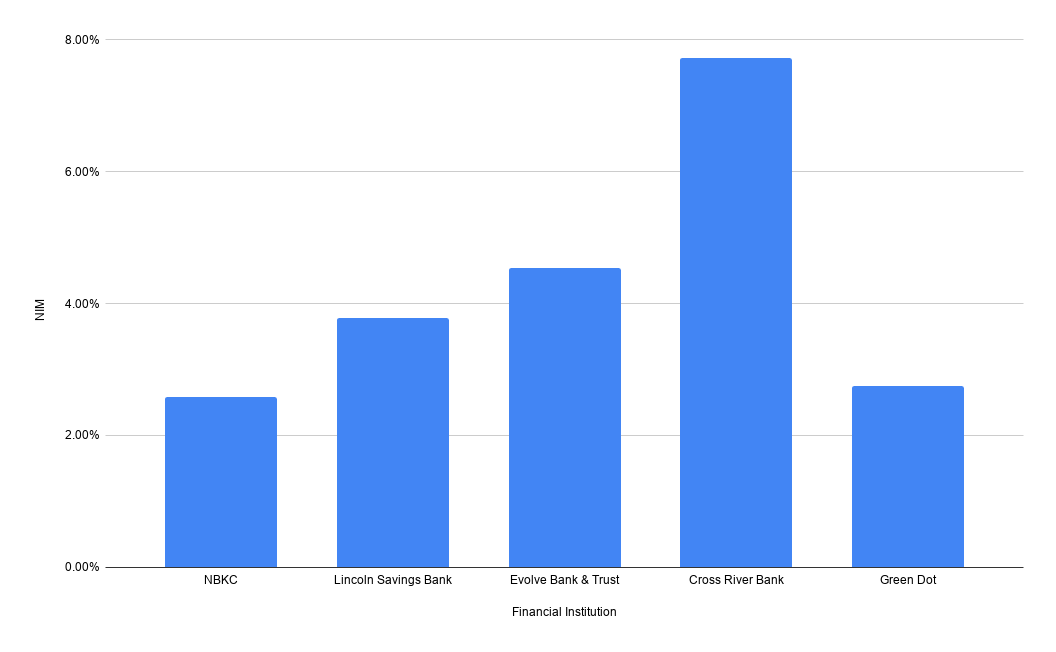

Where does one find bank financials?

You can search for the bank and find Net Interest Margin on the FDIC website. Select the bank and the report to use is Performance and Condition Ratios. Here is the 2019 net interest margin for some common FinTech banks:

Obviously I was lazy and didn’t worry about calculating the 5 year average nor the carry forward trend number for the above image. I thought I’d leave some of that work for you all! Since the data is public you can gather it until your heart is content.

The same data is available for Credit Unions by request through the NCUA website. It took an hour or so for the data I requested to show up in my inbox.

Special Thanks

To a few folks at Eide Bailey who provided some incredibly thoughtful and in depth analysis of this question and everyone who responded to that tweet. A shout out to Jackson Gates who took some time to send some really thoughtful notes.

A Warning

Like my last entry, this type of data could be used with good intentions but dig you a hole if you aren’t careful. NIM over-simplifies things and many FinTech relationships include deposit types and sources which will have different performance. The state of the economy can strongly play into future NIM performance because it’s dependent on the quality of the assets the bank has been investing in.

The best way to get to the bottom of how the bank will make money on a relationship you are building with them is to ask them. Good partnerships are rooted in trust and most banks will just flat out tell you.

What began as kind of a silly tweet gave me some new knowledge. It’s an interesting discussion that helps answer at least one side of the “What is a dollar worth” question which is really “What was an asset worth in past years that a dollar on deposit helped create?” which is a window into how the bank probably thinks about what those dollars will be worth in the future.

The example above is sitting at $100M because it’s the relative scale I think numerous deals are getting done at.