Over the last few months, the team at Brale has been diving deep into DeFi and it’s impossible to avoid the stablecoin discussion. If you google “what is a stablecoin,” the first answer you get is:

Stablecoins are cryptocurrencies. The value of which is pegged, or tied, to that of another currency, commodity or financial instrument. - Source

Under this definition, various forms of stablecoins have been discussed and written about ad nauseam. Takens Theorem has a interesting post on reframing these forms of stablecoins as products.

One of the questions we might begin to ask ourselves is, “why would anyone want a stablecoin or a stable cryptocurrency product?” My answer is an observation, in times of fear, we retreat to safety or a lack of price volatility. In times of excitement, everyone has a number where they get out and lock in their gains. Either way, I find it hard to imagine a world where the majority of future DeFi users 1) don’t know they are using DeFi and 2) price stability of whatever currencies they are using turns out to be an essential feature.

Avoiding for a moment all conversations about reserve currencies and which should be which, I’m going to attempt to move on 🙂

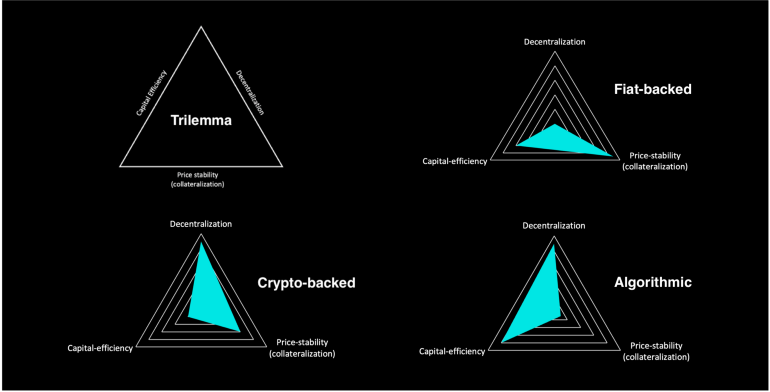

One of the helpful elements of the blog posted above is this image which fairly articulates the attributes of different stablecoins. One of the reasons for the various forms is there are simply multiple approaches to how one might introduce a stable cryptocurrency. Some are far more experimental than others, but all must deal with the challenges of price stability, capital efficiency, and decentralization.

The image above presupposes that decentralization is good and centralization is bad. Much like the initial definition of stablecoin, there is a lot to unpack, and those words can mean different things in different contexts. I often wonder what combination of two is the ideal solution? I’m just not sure we’ve fully seen it yet, making it hard to describe or explain.

If you focus on fiat-backed bucket, you’d probably imagine that definition being different. For example, it might look something like this:

Stablecoins are digital dollars backed 1:1 by government-backed assets held with regulated financial institutions audited by third parties to ensure redeemability.

USDC and USDP fit this critera.

My friend Faisal sometimes describes it as akin to a cashier’s check. Once a regulated entity issues it, the cash is always waiting somewhere when the check is presented on the other side.

The fight over the words is what appears to be a challenge for everyone. When someone says to a consumer the word “stablecoin,” and the consumer makes use of it because of what the perceived purpose of the coin is, that same consumer might use something UST, not knowing what could happen.

If UST is new to you, there are many blogs unpacking this but this is a particularly good one. UST was marketed as a stablecoin, and for those paying close attention to the concept of the algorithmic approach, it was an exciting project. Until it wasn’t, and $50b got wiped out, much of that belonged to regular people who likely have trust issues in the future.

When stuff like this happens, it’s a major trust violation. The whole concept of stability goes away, and when something directionally similar to the size of Enron happens, people will react. People should react.

It’s everywhere:

New York’s financial watchdog issues stablecoin guidance, calls for reserve requirements and audits

LUMMIS, GILLIBRAND INTRODUCE LANDMARK LEGISLATION TO CREATE REGULATORY FRAMEWORK FOR DIGITAL ASSETS

Executive Order on Ensuring Responsible Development of Digital Assets

And it keeps going on and on…

What strikes me as unique is that all of these lawmakers are trying to create a framework that will make it easier and safer for the rest of the world to start using DeFi products. That feels exciting and like a good thing because of what it could mean for DeFi broadly..

A small percentage of people use DeFi products daily, and the presence of a boring stablecoins and various CBDCs seems somewhat inevitable. Some of the more boring products should become easier for businesses and banks to adopt coming out of whatever regulation comes to pass. In that case, it seems to increase the likelihood that a growing percentage of people will get access to these technologies.

Boring can be good.