At Money 20/20 last week, a topic that came up over and over in discussions was blockchain performance compared to traditional databases used to ledger transactions. One must be excellent at double-entry bookkeeping and performant state machines to use a traditional database to ledger transactions.

The overwhelming majority of banks and FinTechs use this approach and spend a great deal of time on it. Their business depends on it. It is the backbone of the balances we all see in our bank accounts and every popular FinTech app I can think of.

Blockchains, built correctly, can make this much simpler by design.

Three things feel worth appreciating when thinking about this in the current environment.

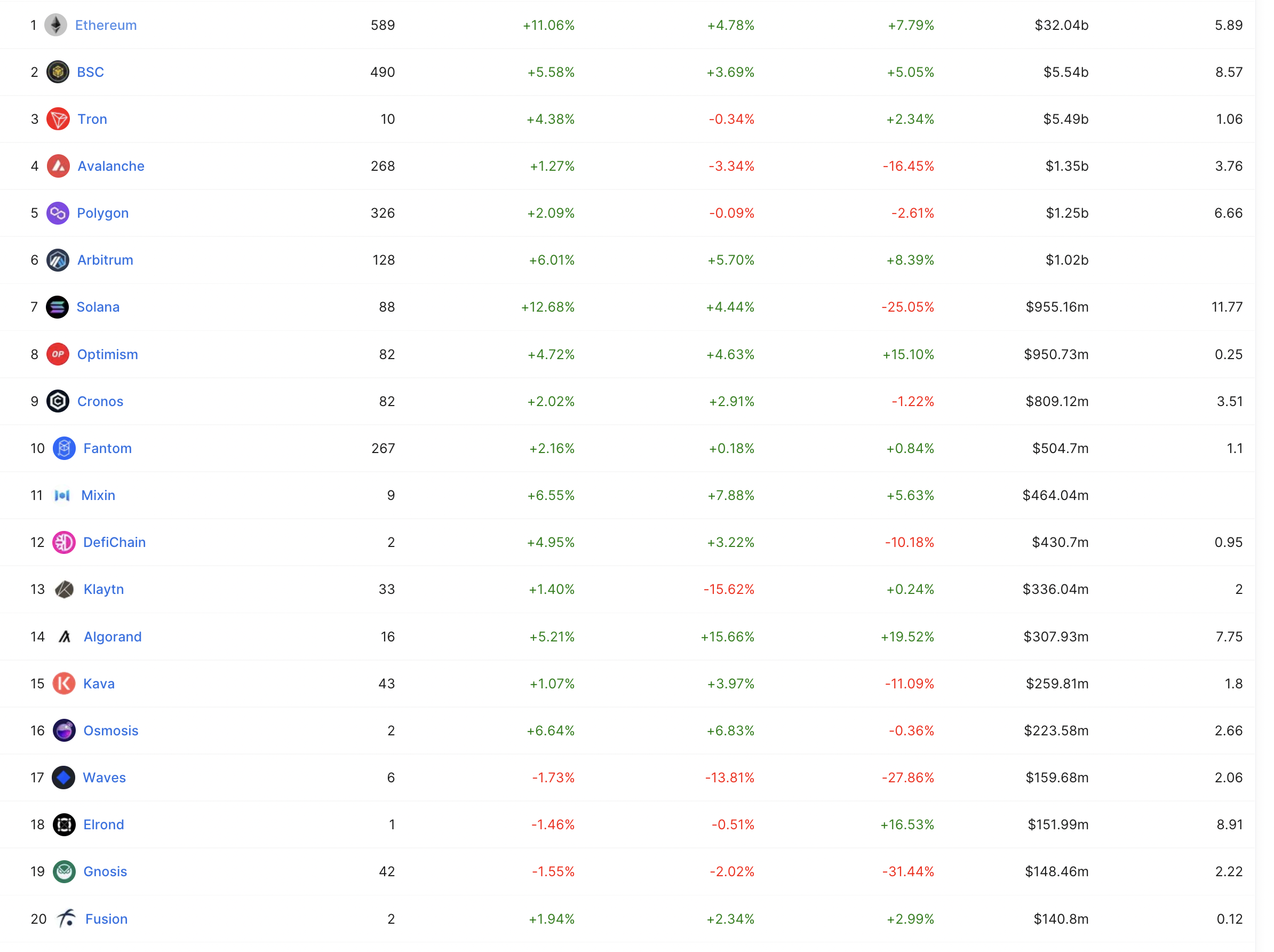

First – If we look at the balances held in financial institutions on behalf of Fintech clients, where purpose-built balances are recorded, several FinTechs would be top10 chains alone if they were themselves a chain. They are not chains – they are built on databases that track the state of a balance, resulting in permission-based balances. Looking at the TVL in top chains 2-10, it’s easy to imagine some FinTechs that are larger.

The technology market does not see FinTech TVL in these graphs so it is forgotten in the conversation. The takeaway is that the balances of popular FinTech and bank products are not reflected in on-chain data or well understood. The lack of understanding leads to a further lack of understanding of how big FinTech is from a balance or deposit perspective.

If TVL can be considered comparable to AUM, then even Ethereum has a long way to go. These chains have so much room to keep growing.

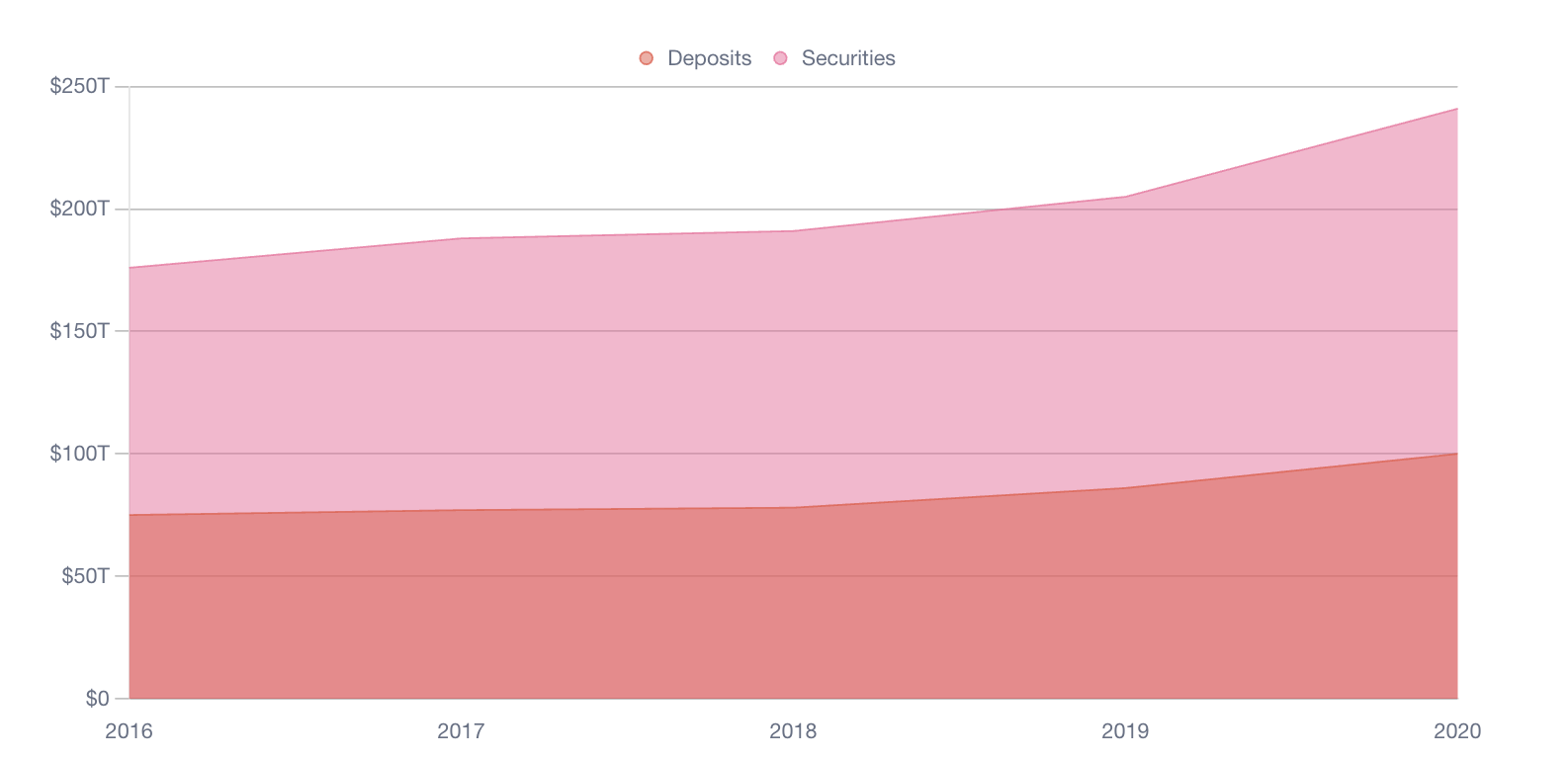

Second – The majority of the world’s capital is off-chain. There are hundred(s) of trillions in the world’s financial institutions primarily stored off-chain. Just like the FinTech balances I mentioned previously, these balances are often forgotten. If we ignore throughput and focus on the amount, it is stunning how big the numbers are.

Third – The choices made in tracking balances in massively scalable applications are changing. Some teams have to worry about TPS, maybe in the millions per second. If you are not worried about throughput TPS in the millions, you are in the majority of most software applications. Even many successful FinTech companies are in the millions per month range–a far cry from millions per second.

When considering atomic assets that can move across chains, the concept of sharding assets across chains to optimize for available TPS is just payment orchestration in a chain context. That may be separate from the design for something like USDC, for example, but in a multi-chain world, it could be interesting.

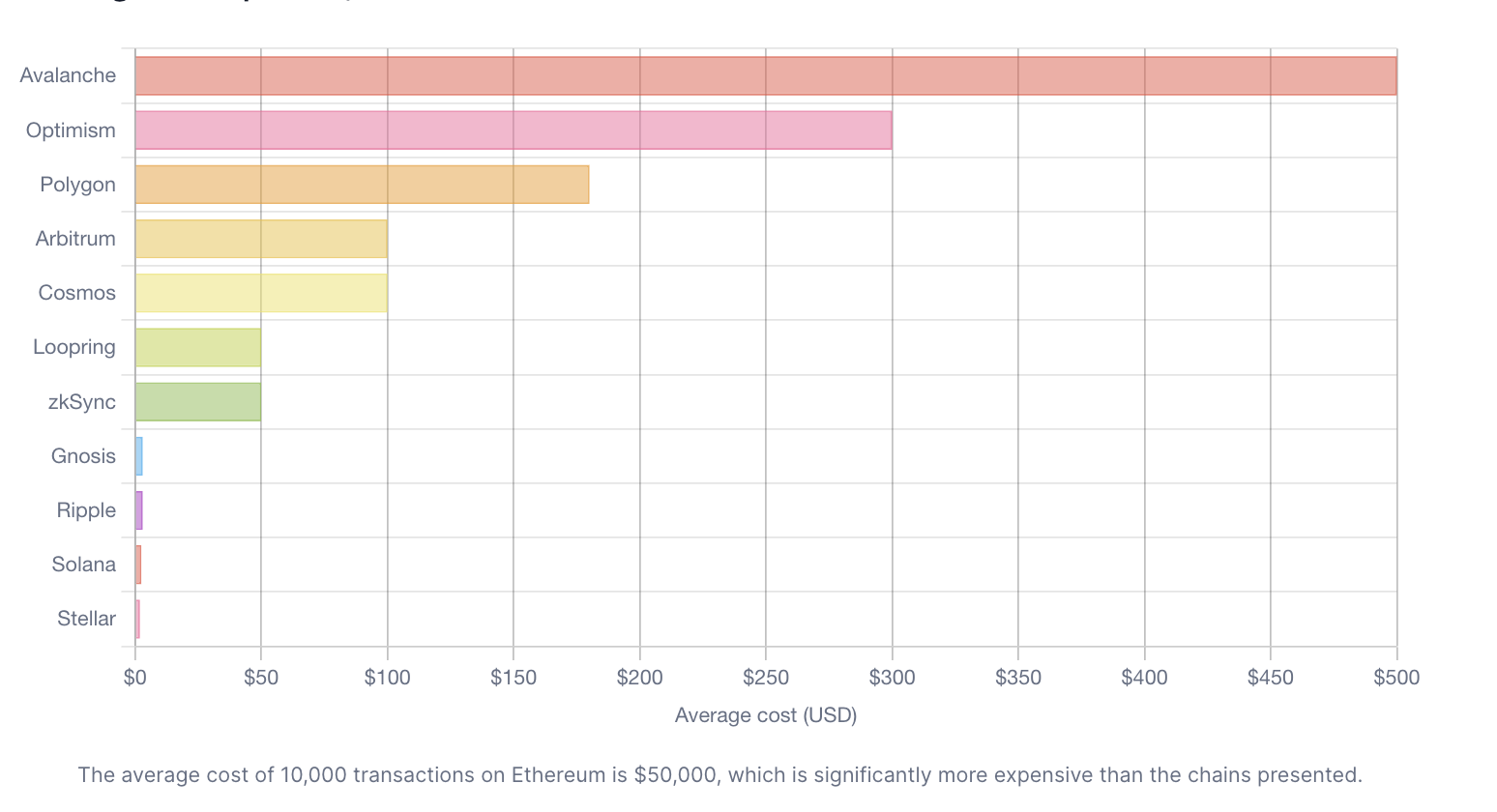

Considering the cost of operating a well-designed ledgering infrastructure on AWS or Azure, supporting a few million transactions per month with perfect accounting gets expensive quickly. Same with some chains but not so much with others, as is shown below.

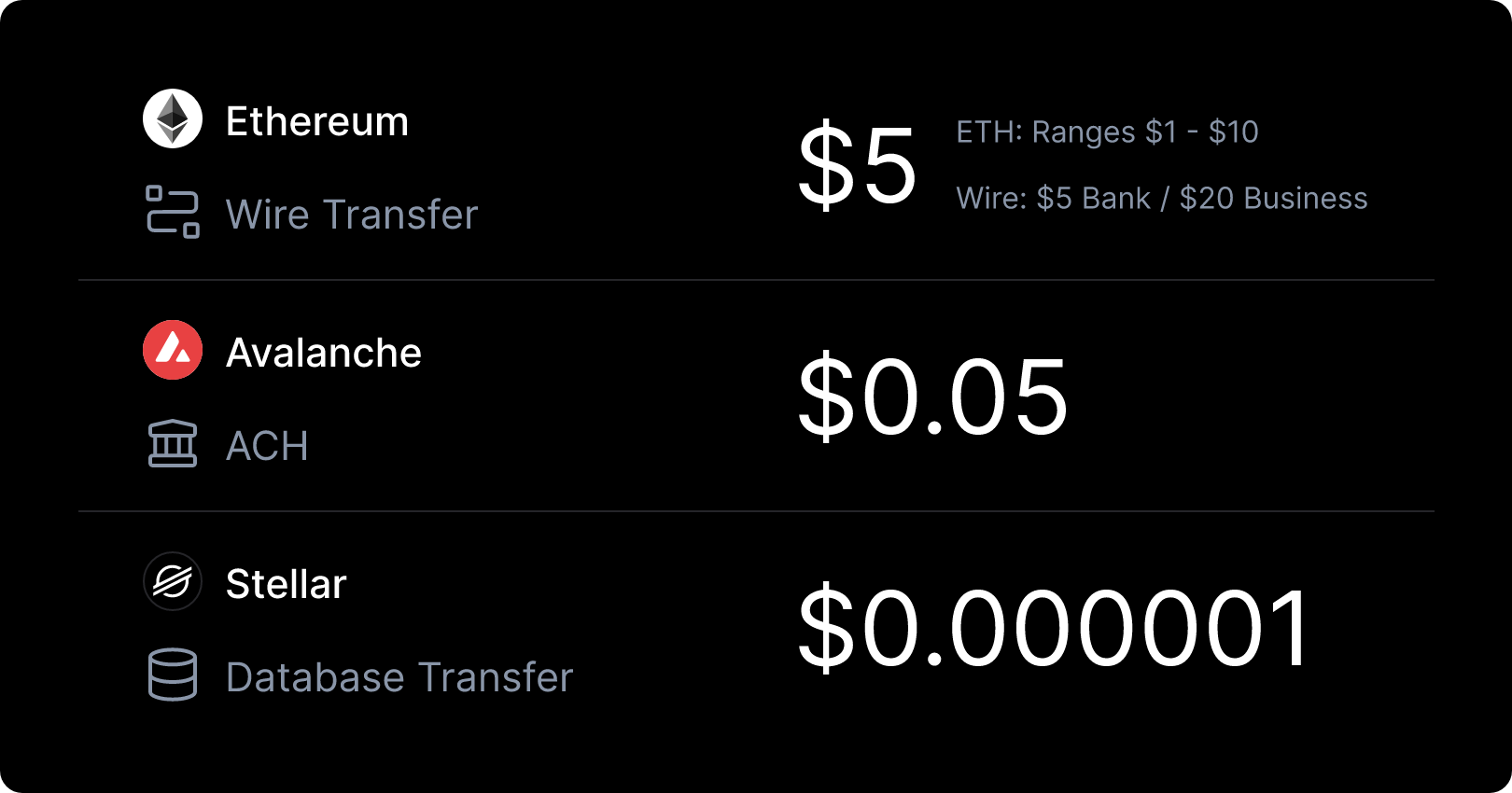

From a cost perspective, things go from not bad to incredible in this analysis alone. $50,000 on one chain compared to less than $1 on another to complete and record a transfer is eye-opening. Remember that $5 for a final, real-time, globally capable transaction is pretty good, and that is the starting point!

The idea of ledgering 1 million transactions for $1 without worrying about accuracy seems hard to believe, but here we are. Considering the cost of transfer compared to traditional forms of transfer in the United States, it is a bit of a mind-bender.

Accounting systems are essential in banks and finance, but the technology, quality, and costs available now were virtually impossible 10 years ago.

The discoveries are eye-opening if we dare to test the distributed systems in front of us. Cost is only one of the considerations, but the scales may have tipped.

That is exciting.

Acknowledgments

To the entire Brale team who has done important exploration on these topics. Without the team’s contributions and insights I wouldn’t have these thoughts to share.

To the Money 20/20 team for being the motivation to write some of the recent blogs and being the impetus for the discussions that took place last week.